Lifetime ISA vs ISA: which one suits your savings goals?

Choosing between a Lifetime ISA and a regular ISA depends on your age, goals and risk tolerance. A Lifetime ISA offers a 25% government bonus for first home buys or retirement, but comes with strict withdrawal rules, while regular ISAs provide more flexibility without bonuses. In 2025, the total ISA allowance is £20,000, with Lifetime ISAs capped at £4,000 contributions for the bonus. This comparison helps you decide based on lifetime isa vs isa needs, whether for home buying or general savings.

What is a Lifetime ISA?

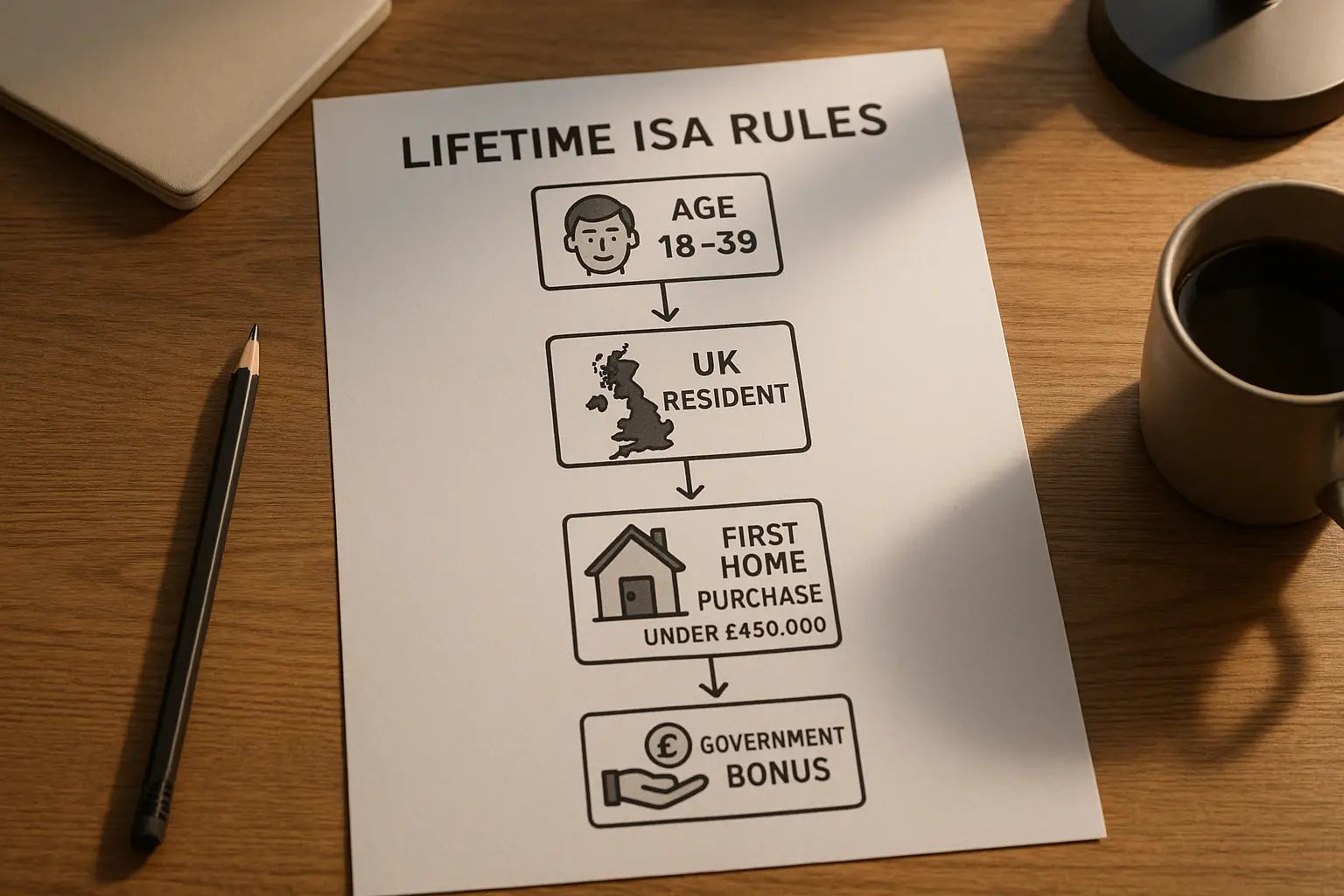

The core benefit of a Lifetime ISA is the government top-up, making it ideal for long-term savers aged 18-39. Unlike regular options, it locks in funds until age 60 or a first home purchase, with penalties for early access.

Eligibility and contribution rules

You must be a UK resident aged 18 to 39 to open a Lifetime ISA, and you can contribute until age 50. The annual limit is £4,000, part of the overall £20,000 ISA allowance for 2025-26. For example, if you add £4,000, the government adds £1,000 instantly. Check eligibility details on the official GOV.UK Lifetime ISA page.

Government bonus explained

The 25% bonus applies to contributions up to £4,000 yearly, maxing at £1,000 free money. This boosts home deposits or retirement pots significantly—over 10 years, £40,000 saved could become £50,000 with bonuses. As per MoneySavingExpert, this incentive has helped 87,250 people buy first homes in 2024-25.

Withdrawal options and penalties

Withdraw penalty-free for a first home under £450,000 or after 60. Otherwise, a 25% charge applies, clawing back the bonus plus 6.25% of your input. In 2023-24, average withdrawals for homes rose 8% to support deposits, according to AJ Bell research.

What is a regular ISA?

Regular ISAs are flexible tax-free wrappers for cash or investments, without age limits or bonuses. They suit short-term savers or those avoiding restrictions, offering easy access across various types.

Types of regular ISAs: cash and stocks and shares

Cash ISAs provide low-risk savings with interest up to 4.30% AER in 2025, similar to a bank account. Stocks and shares ISAs invest in funds or shares for potential higher returns (historically 5-7% annually), but with market volatility. Lifetime isa vs cash isa often favours cash for safety, while lifetime isa vs stocks and shares isa highlights growth potential with bonuses.

Annual allowance and flexibility

You can invest up to £20,000 across all ISAs yearly, with no withdrawal penalties. Split between cash and stocks as needed—perfect for emergencies. Unlike Lifetime options, no age caps mean accessibility for all adults.

Tax benefits

All growth, interest and dividends are tax-free forever. For higher-rate taxpayers, this saves up to 40% on gains, making ISAs a smart hack vs taxable accounts.

| Feature | Lifetime ISA | Regular ISA |

|---|---|---|

| Contribution limit | £4,000 (bonus eligible) | Up to £20,000 |

| Government bonus | 25% on contributions | None |

| Withdrawal flexibility | Restricted (penalties apply) | Any time, no penalty |

| Best for | Home/retirement (18-50) | General savings/investments |

| Risk level | Low to high (cash/stocks variants) | Low to high |

Lifetime ISA vs Help to Buy ISA

The Help to Buy ISA is a legacy scheme closed to new savers since 2019, but Lifetime ISAs have replaced it with better bonuses for new entrants. If you have an old Help to Buy, you can transfer to a Lifetime for ongoing benefits.

Key similarities and differences

Both target first-time buyers with government top-ups: Help to Buy gave 25% on £12,000 max (£3,000 bonus), but only for homes up to £250,000 (now £450,000 for Lifetime). Lifetime isa vs help to buy isa shows Lifetime’s higher limits and dual use for retirement. Help to Buy withdrawals are now limited, per Which? guides.

Pros and cons for first-time buyers

- Lifetime pros: Higher bonus cap, stocks option for growth, retirement fallback.

- Lifetime cons: Age restrictions, 25% penalty if plans change.

- Help to Buy pros: Existing holders keep bonuses, no age limit for transfers.

- Help to Buy cons: No new entries, lower property cap.

For lifetime isa vs help to buy, switch if eligible for bigger incentives.

Transition from Help to Buy

Transfer your Help to Buy balance to a Lifetime ISA without losing bonuses—providers like Moneybox handle this. In 2025, this hack maximises your deposit, as Martin Lewis advises on MoneySavingExpert.

Lifetime ISA vs stocks and shares ISA or cash ISA

Stocks and shares ISAs offer higher potential returns without bonuses, suiting risk-takers, while cash versions match Lifetime cash safety but add flexibility. Choose based on lifetime isa vs stocks and shares isa for growth or isa vs lifetime isa for access.

Risk and return comparison

Cash Lifetime ISAs yield 4.30% AER safely, but stocks variants could grow faster (5-7% long-term). Regular stocks ISAs avoid penalties, ideal if unsure about home buys. Per Moneyfacts, cash isa vs lifetime isa prioritises liquidity over bonuses.

Flexibility and use cases

Regular ISAs allow full £20,000 use freely; Lifetime locks most funds. For first homes, Lifetime’s bonus wins; otherwise, regular for versatility.

Quick tips for smarter ISA choices

- Assess goals: Home soon? Go Lifetime. Flexible needs? Regular cash.

- Max the bonus: Contribute £333 monthly to hit £4,000 yearly.

- Compare providers: Use best Lifetime ISA rates guide for low fees.

- Diversify: Mix Lifetime with regular for balanced savings.

- Avoid penalties: Plan withdrawals carefully or face 25% hit.

Lifetime ISA vs SIPP or pension

SIPPs offer tax relief up to 45% on contributions but lock funds until 55, unlike Lifetime’s earlier access for homes. Lifetime isa vs sipp balances bonus vs relief; pensions suit retirement-focused savers.

Tax incentives and access

SIPPs give upfront relief (e.g., £100 becomes £125 for basic taxpayers), growing tax-free. Lifetime’s 25% is on input only. Withdrawal: Pensions at 55+, Lifetime at 60 or home buy. For lifetime isa vs pension, combine both for optimal retirement.

Risks and strategies

SIPPs have investment risks like Lifetime stocks, but higher limits (£60,000/year). Expert tip: Higher-rate taxpayers may prefer SIPP’s relief over Lifetime bonus, as discussed in Money to the Masses comparisons.

Alternative savings options

Compare Lifetime isa vs premium bonds for low-risk fun (no interest, prize draws) or lifetime isa vs overpay mortgage to cut debt faster. Overpaying saves interest (e.g., 4-5% effective return), but lacks tax-free growth. For parents, skip child-focused like junior ISA vs lifetime isa—Lifetime is adult-only.

Best Lifetime ISA providers offer competitive rates; explore what is a Lifetime ISA basics first. Lifetime ISAs returned £1bn to the Treasury since 2021, per The Intermediary, showing strong uptake.

Frequently asked questions

What is the difference between a Lifetime ISA and a regular ISA?

A Lifetime ISA targets long-term goals like buying a first home or retirement, offering a 25% government bonus on up to £4,000 yearly contributions, but with withdrawal penalties before age 60 or for non-qualifying uses. Regular ISAs, including cash and stocks and shares types, provide tax-free savings up to £20,000 annually without bonuses or restrictions, allowing flexible access anytime. The key distinction in lifetime isa vs isa lies in the incentive for specific milestones versus broad, penalty-free saving, making regular ISAs better for short-term needs while Lifetime suits committed long-haulers aged 18-39.

Is a Lifetime ISA better than a stocks and shares ISA?

For first-time home buyers or retirement savers under 50, a Lifetime ISA often edges out due to the 25% bonus, potentially adding £1,000 yearly on top of investment growth. However, stocks and shares ISAs allow full £20,000 contributions with no age limits or penalties, suiting those wanting higher exposure without locks. In lifetime isa vs stocks and shares isa scenarios, assess risk tolerance—Lifetime’s bonus amplifies returns but penalties deter if plans change, while regular investments offer pure flexibility for diversified portfolios.

Can I have a Lifetime ISA and a regular ISA?

Yes, you can hold both, as the Lifetime ISA’s £4,000 contribution counts toward your total £20,000 ISA allowance, leaving room for regular cash or stocks ISAs. This strategy maximises bonuses while maintaining liquidity elsewhere. For instance, use Lifetime for home goals and a cash ISA for emergencies; always track allowances via HMRC to avoid over-contributing and losing tax benefits.

What happens if I withdraw from a Lifetime ISA before 60?

Non-qualifying withdrawals incur a 25% penalty, recovering the government bonus and an extra 6.25% from your savings, potentially leaving you worse off. Qualifying uses—no penalty—include first home buys under £450,000 or post-60 access. Experts recommend avoiding early draws; if circumstances change, transfer to a regular ISA to dodge charges, as outlined by GOV.UK rules.

Is the Help to Buy ISA still available, and how does it compare to Lifetime ISA?

New Help to Buy ISAs closed in 2019, but existing ones remain active for contributions until exhausted. Lifetime ISA has superseded it with a higher £450,000 property cap and dual home/retirement use, plus the same 25% bonus on £4,000. In lifetime isa vs help to buy isa, transfer old balances to Lifetime for continued growth, boosting deposits—Martin Lewis highlights this as a top hack for buyers.

Lifetime ISA vs SIPP: which is better for retirement?

SIPPs excel with upfront tax relief (20-45% boost) and higher limits, ideal for higher earners planning solely for retirement from age 55. Lifetime ISAs add a 25% bonus and earlier home access, but cap at £4,000 and penalise non-retirement withdrawals before 60. For advanced strategies in lifetime isa vs sipp, blend them—use SIPP for tax efficiency and Lifetime for bonus-enhanced pots, monitoring fees and risks for optimal long-term yields.

Should I choose Lifetime ISA over mortgage overpayments?

Mortgage overpayments reduce interest (effective 4-6% return, tax-free), suiting low-rate debtors for quick equity build. Lifetime ISAs offer 25% bonus plus potential 4.30% cash rates or stock growth, but with penalties if not used for home/retirement. In lifetime isa vs overpay mortgage, prioritise overpayments if rates exceed ISA yields or debt is high-interest; otherwise, Lifetime accelerates deposits for under-£450,000 homes, per Which? advice.