What is a Lifetime ISA?

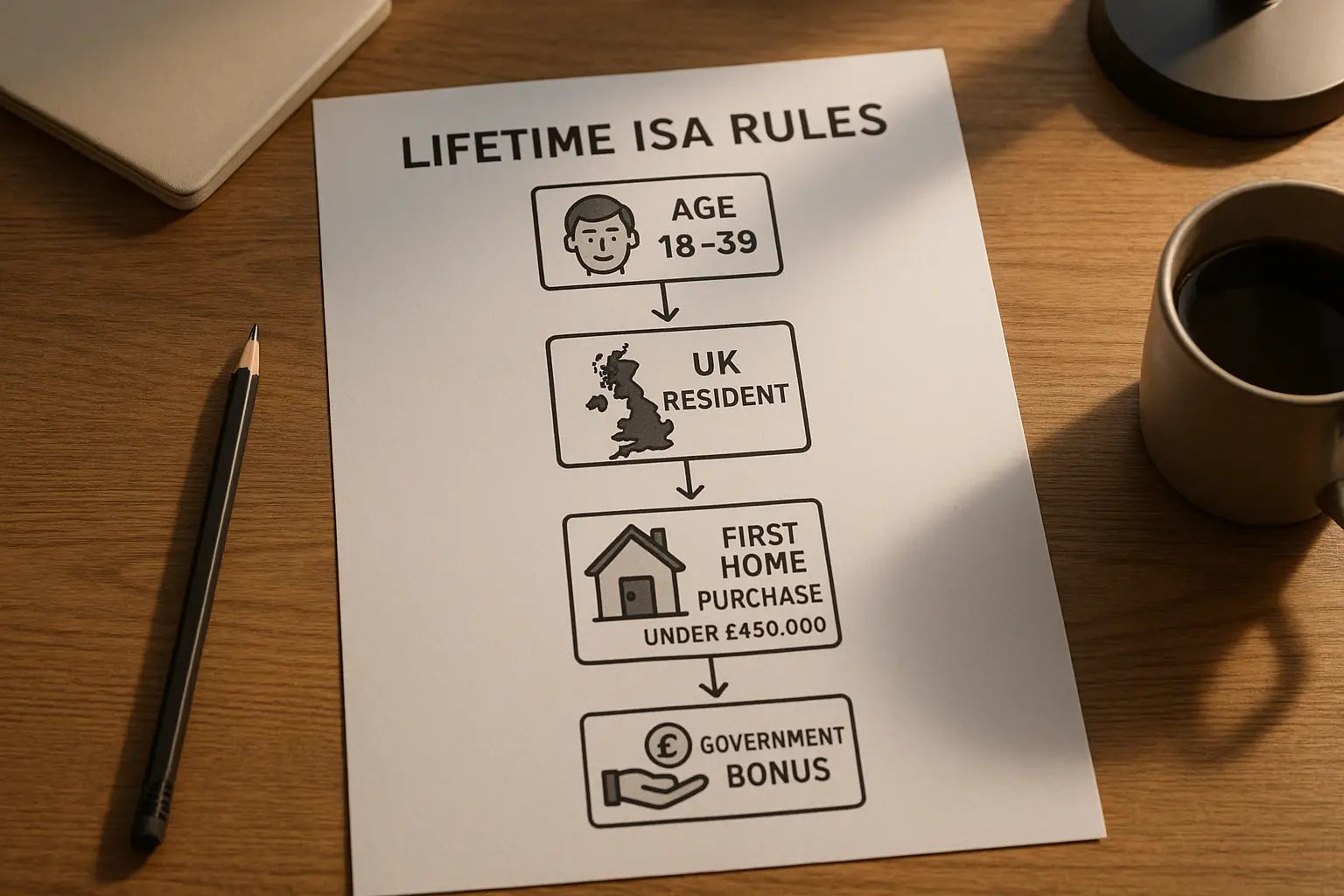

A Lifetime ISA, often abbreviated as LISA, is a tax-free savings account designed to help UK residents aged 18 to 39 save for their first home or retirement. Introduced in 2017, it combines the benefits of a standard Individual Savings Account (ISA) with a generous government bonus to encourage long-term saving. Unlike regular ISAs, a Lifetime ISA has specific rules tied to its purposes, making it a smart choice for first-time buyers or those planning ahead for later years.

Eligibility and who can open one

To open a Lifetime ISA, you must be aged 18 to 39 and a UK resident. You can continue contributing until age 50, even if you open it later in that range. UK residency is key, as defined by HMRC rules, and non-residents may face restrictions. If you’re unsure about your status, check the official guidance on GOV.UK’s eligibility page. This setup targets young adults starting their financial journey, helping avoid common saving pitfalls like low-interest accounts.

Purpose for first home or retirement

The core purpose of a Lifetime ISA is to support buying your first home worth up to £450,000 or saving for retirement from age 60. It’s ideal if you’re dreaming of homeownership but facing high deposits, or want a boosted pension pot. Since launch, over 500,000 accounts have been opened, with average balances reaching £5,200 by 2024, showing its popularity among savvy savers (source: Moneybox report, 2025). By focusing on these goals, it prevents the mistake of scattering savings across ineffective options.

How does a Lifetime ISA work?

A Lifetime ISA works by allowing tax-free contributions that grow without capital gains or income tax, plus a 25% government top-up on your savings each year. You can open one from age 18, contribute up to the annual limit, and the government adds its bonus automatically via your provider. For those wondering what is a Lifetime ISA account, it’s essentially a specialised ISA wrapper around cash or investments, tailored for life milestones.

Contributions and tax year rules

Contributions are limited to £4,000 per tax year, running from 6 April to 5 April, and this counts towards the overall £20,000 ISA allowance for 2025/26 (source: Moneybox, 2025). You can contribute in lumps or regularly, and some providers offer flexible rules allowing withdrawals and replacements within the same year without affecting the bonus. Start small to build the habit—many users on social media share how monthly £100 contributions snowballed into significant deposits.

Government bonus explained

The government bonus is 25% of your contributions, up to £1,000 per year on a maximum £4,000 saved. For example, save £4,000 and get £1,000 free, making £5,000 total. This what is a Lifetime ISA bonus query is common, as it effectively boosts your saving power instantly. The bonus appears within 30 days and is claimable once the account is open for a year, per GOV.UK rules.

Types: Cash vs stocks and shares

There are two main types: a cash Lifetime ISA, like a high-interest savings account with fixed or variable rates (what is a cash Lifetime ISA?), offering stability but lower returns around 4-5% currently. A stocks and shares Lifetime ISA invests in funds or shares for potentially higher growth, but with market risk (what is a stocks and shares Lifetime ISA?). Flexible Lifetime ISAs allow same-year withdrawals without penalty. Choose based on your risk tolerance—cash for safety, investments for growth.

Benefits of a Lifetime ISA

The standout benefit is the 25% bonus turning your savings into more without extra effort, alongside tax-free growth that beats standard accounts. For UK savers, it’s a hack to stretch deposits further amid rising costs.

25% bonus and tax advantages

Beyond the bonus, all interest, dividends, and gains are tax-free, unlike non-ISA savings hit by the £1,000 personal savings allowance. What is the interest rate on a Lifetime ISA? It varies by provider, but cash versions often match or exceed standard ISAs at 4-5%, while stocks aim for 5-7% long-term average. This combo has delivered £1 billion net gain to the Treasury since 2017, but huge value to users (source: The Intermediary, 2025).

Long-term growth potential

Over time, compounding in a Lifetime ISA can build substantial wealth. For instance, £4,000 annual contributions at 5% return could grow to over £70,000 in 10 years. It’s perfect for retirement or home goals, with projections showing up to £4 billion Treasury impact by 2040, underscoring its scale.

| Aspect | Details (2025/26) | Source |

|---|---|---|

| Annual Contribution Limit | £4,000 | GOV.UK |

| Government Bonus | 25% up to £1,000 | GOV.UK |

| Overall ISA Allowance | £20,000 | Moneybox |

| Age to Contribute Until | 50 | MoneySavingExpert |

Rules, limits, and withdrawal penalties

Key rules include the £4,000 cap and penalty-free access only for approved uses. What are Lifetime ISA rules? They ensure savings stay goal-focused, with breaches costing you.

Annual and lifetime limits

Annually, £4,000 max, no lifetime cap on total savings but contributions stop at 50. The ISA limit 2025 remains £20,000 overall, so balance with other ISAs wisely. What is the maximum you can put in a Lifetime ISA? Just that £4,000 yearly slice.

When you can withdraw penalty-free

Withdraw tax-free at 60 for any purpose, or after one year for a first home under £450,000. Transfers from Help to Buy ISAs are allowed, preserving bonuses (source: MoneySavingExpert, 2025). Terminal illness exemptions also apply, waiving penalties.

What happens if you break the rules

Non-permitted withdrawals incur a 25% penalty on the entire amount, clawing back the bonus plus 6.25% of your money. What is a Lifetime ISA withdrawal penalty? It’s steep—losing £1,250 on a £5,000 pot—to discourage early dips. Always plan ahead to avoid this trap.

Lifetime ISA providers and how to open one

Providers like Moneybox, HSBC, and Nationwide offer these accounts; what is a Lifetime ISA Moneybox? It’s a popular app-based option with easy setup. For the best Lifetime ISA rates, compare via trusted sites without deep dives here.

Key providers overview

Options include banks (HSBC for cash security) and platforms (Hargreaves Lansdown for investments). Martin Lewis recommends checking MoneySavingExpert for updates. Lifetime ISA providers vary in fees and returns—pick based on your type.

Steps to apply

1. Confirm eligibility on GOV.UK.

2. Choose cash or stocks via a provider’s site.

3. Provide ID and set up contributions.

4. Watch for the bonus arrival. It’s straightforward, often online in minutes.

For more on types of ISAs in the UK, explore our savings guide. Ready to save smarter? Visit GOV.UK to get started.

Frequently asked questions

Who is eligible for a Lifetime ISA?

Eligibility for a Lifetime ISA requires you to be 18-39 years old and a UK resident at the time of opening. You can keep contributing until 50 if you start earlier. This targets young adults saving for big goals, but expatriates or those under 18 can’t participate. Check residency via HMRC to avoid application denials, as rules ensure it’s for UK-based savers building long-term security.

What is the government bonus on a Lifetime ISA?

The government bonus on a Lifetime ISA is 25% of your annual contributions, capped at £1,000 for £4,000 saved. It’s paid automatically by your provider after verification. This incentive, unchanged for 2025/26, boosts first-home deposits or retirement funds effectively. Unlike other bonuses, it’s tax-free and claimable after one year, making it a key draw for beginners.

What happens if you withdraw from a Lifetime ISA?

If you withdraw from a Lifetime ISA for non-approved reasons, like general spending, you’ll face a 25% penalty on the full balance including bonus. This recovers the government’s contribution plus a slice of yours, often around 6.25% loss on your input. Exceptions exist for age 60+ or terminal illness, allowing penalty-free access. Always review rules to prevent costly mistakes in your saving strategy.

Can you transfer a Help to Buy ISA to a Lifetime ISA?

Yes, you can transfer a Help to Buy ISA to a Lifetime ISA, moving your savings and any prior bonuses intact. The process is provider-handled, preserving tax-free status and adding the new 25% top-up. This is useful post-Help to Buy closure in 2021, extending benefits for homes up to £450,000. Time it within tax years to maximise allowances, consulting MoneySavingExpert for seamless steps.

What is the difference between cash and stocks Lifetime ISA?

A cash Lifetime ISA holds money in savings-like accounts with fixed interest, low risk but modest returns around 4%. A stocks and shares version invests in markets for higher potential gains (5-7% average), but value can fluctuate. Both get the bonus, but cash suits cautious savers, while stocks fit those comfortable with volatility for retirement. Diversify based on goals to balance safety and growth.

Can I lose money in a Lifetime ISA?

In a cash Lifetime ISA, your money is protected up to £85,000 per provider via FSCS, so no loss from insolvency, though inflation might erode value. Stocks and shares versions can lose capital if markets dip, unlike guaranteed cash rates. For 2025, historical data shows long-term recovery, but short-term risks apply. Assess your timeline—over 5+ years, stocks often outperform, per expert analyses from The Telegraph.

What is the purpose of a Lifetime ISA?

The purpose of a Lifetime ISA is to help UK residents save tax-free for a first home under £450,000 or retirement from 60, with a 25% government boost. It addresses affordability challenges for young buyers and pension gaps. Since 2017, it’s encouraged disciplined saving, with over 500,000 accounts aiding real goals. Use it strategically to avoid scattering funds across less efficient options.

Word count: 812