Understanding Lifetime ISA basics

A Lifetime ISA (LISA) is a tax-free savings account designed to help UK residents aged 18 to 39 save for their first home or retirement, with the government adding a 25% bonus on contributions up to £1,000 annually. This makes it a powerful tool for long-term goals, but withdrawing funds incorrectly can trigger lifetime ISA withdrawal penalties that wipe out gains and more. To avoid costly mistakes, grasp the basics before committing your money.

What is a Lifetime ISA?

The core of a Lifetime ISA is its dual purpose: funding a first home deposit or supplementing retirement savings after age 60, all while growing tax-free. Unlike standard savings accounts, it locks in your money until qualifying events to encourage disciplined saving. For beginners, think of it as a boosted piggy bank where the government chips in, but early access comes at a price—often the focus of searches on lifetime ISA early withdrawal penalties.

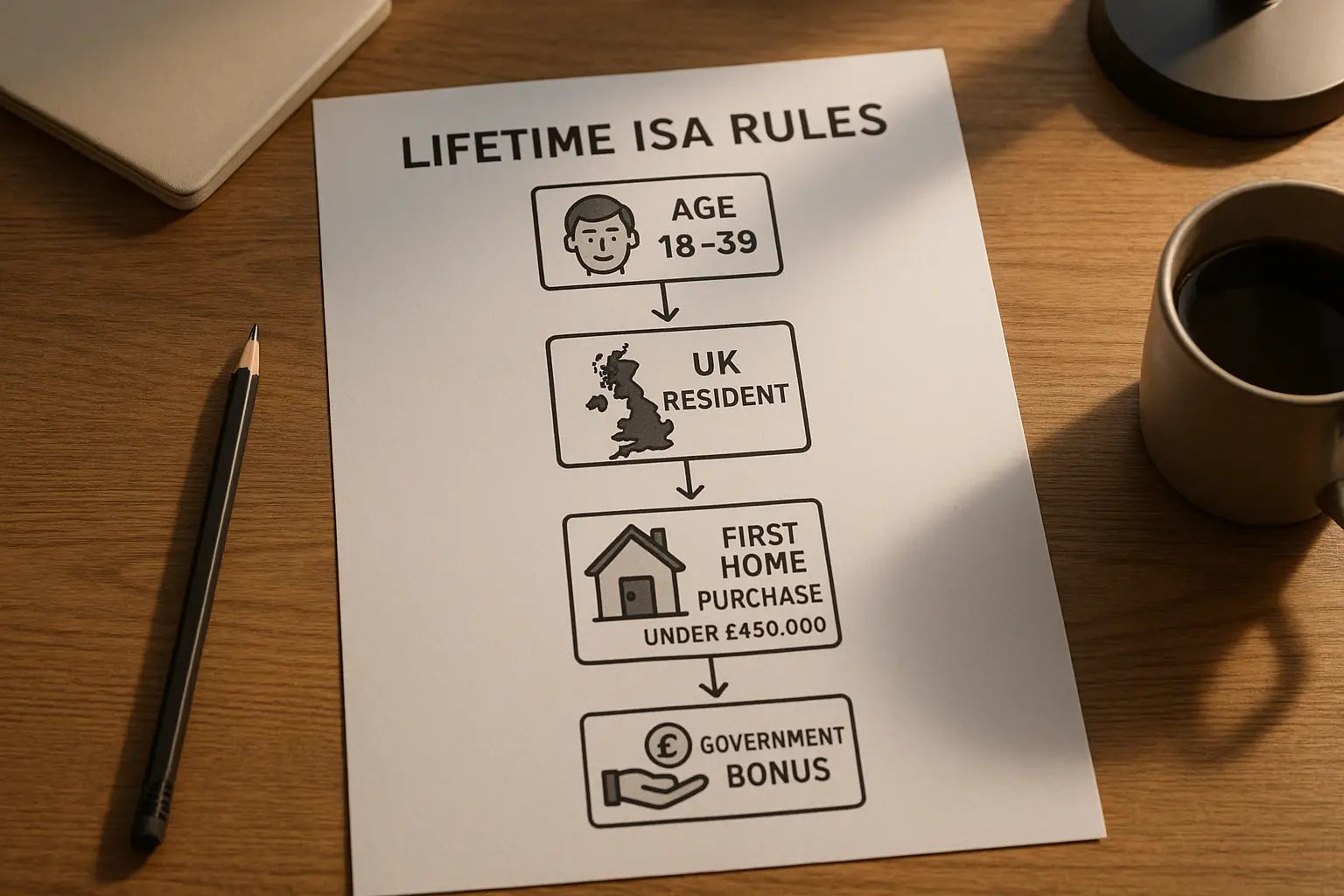

Government bonus and eligibility

Eligibility requires you to be 18-39 when opening, a UK resident, and not previously held a LISA; you can contribute until 50. The government bonus matches 25% of your deposits, up to £4,000 yearly, turning £3,200 saved into £4,000 instantly. This incentive is why lifetime ISA withdrawal penalties UK sting so much—they can claw back the bonus plus your own cash if rules are broken.

Key differences from other ISAs

Unlike a standard ISA, which allows penalty-free withdrawals anytime, a LISA imposes strict rules to protect the bonus, making it less flexible but more rewarding for homebuyers. Cash LISAs earn interest, while stocks and shares versions offer growth potential with risk. If flexibility matters, compare via our guide on lifetime isa vs isa, but for home savers, LISA’s bonus edges out.

Permitted withdrawals without penalty

You can withdraw from a Lifetime ISA penalty-free for buying your first home (up to £450,000), reaching age 60, or in terminal illness cases—core exceptions that safeguard your savings for intended uses. These rules prevent lifetime ISA withdrawal penalties when followed, ensuring you keep the full amount including bonus. Always verify with your provider to confirm eligibility and avoid surprises.

First home purchase rules

To use LISA funds penalty-free for a first home, the property must cost £450,000 or less, you must be a first-time buyer (no prior ownership), and complete the purchase within 90 days of withdrawal. This exception targets the housing ladder climb, a common goal for 18-39-year-olds. Exceeding the price cap triggers HMRC lifetime ISA withdrawal penalties, so check market values first—what counts as a first home purchase includes shared ownership but not buy-to-let.

Withdrawals after age 60

Once you turn 60, all LISA funds become fully accessible tax-free, with no withdrawal limits or penalties, ideal for retirement planning. This aligns with pension-like benefits, allowing you to draw down as needed without losing the government bonus. Plan ahead: contributions stop at 50, but growth continues, making age 60 a penalty-free milestone.

Terminal illness exception

If diagnosed with less than 12 months to live (certified by a doctor), you can withdraw everything penalty-free at any time. This compassionate rule overrides age or home restrictions, prioritizing access in hardship. Contact HMRC or your provider promptly to process this exception without incurring lifetime ISA withdrawal penalties UK.

Non-permitted withdrawal penalties

Non-permitted withdrawals before age 60 incur a 25% HMRC charge on the entire amount, including your contributions and bonus, effectively returning you to pre-bonus levels but penalizing extra. This lifetime ISA withdrawal penalties structure deters casual access, with enforcement by providers reporting to HMRC. In 2024/25, these charges hit £102 million across 129,000 savers, up 35% from £75.5 million the year before (source: Mortgage Solutions).

How the 25% charge works

The penalty deducts 25% from the withdrawn sum—your money plus bonus—meaning if you take out £4,000 (from £3,200 saved + £800 bonus), HMRC takes £1,000, leaving £3,000. This exceeds the bonus clawback to discourage misuse, as per official rules (source: GOV.UK). For example, early withdrawals for non-home expenses like holidays trigger full lifetime ISA early withdrawal penalties.

| Scenario | Deposit | Bonus | Total | Penalty (25%) | Net Received |

|---|---|---|---|---|---|

| Permitted: First home £400,000 | £3,200 | £800 | £4,000 | £0 | £4,000 |

| Non-permitted: Emergency cash | £3,200 | £800 | £4,000 | £1,000 | £3,000 |

| Age 60 withdrawal | £3,200 | £800 | £4,000 | £0 | £4,000 |

HMRC enforcement process

Providers automatically apply the 25% charge and remit it to HMRC, who oversees compliance as the UK’s tax authority. You receive the net amount, and non-payment can lead to further fines or audits. For details on HMRC lifetime ISA withdrawal penalties, appeal via your provider if errors occur.

Recent penalty trends and statistics

Penalties soared to £102 million in 2024/25, affecting 129,000 savers amid housing woes (source: The Independent). The prior year saw £75 million for nearly 100,000 people (source: GB News), highlighting a rising trend. These lifetime ISA withdrawal penalties UK figures fuel reform debates, as first-time buyers struggle.

Avoiding and appealing penalties

To dodge penalties, stick to permitted uses or transfer to another ISA before withdrawing—proactive steps that preserve your savings. If charged wrongly, appeal to HMRC within 30 days for refunds. Stay informed on changes to navigate lifetime ISA withdrawal penalties safely.

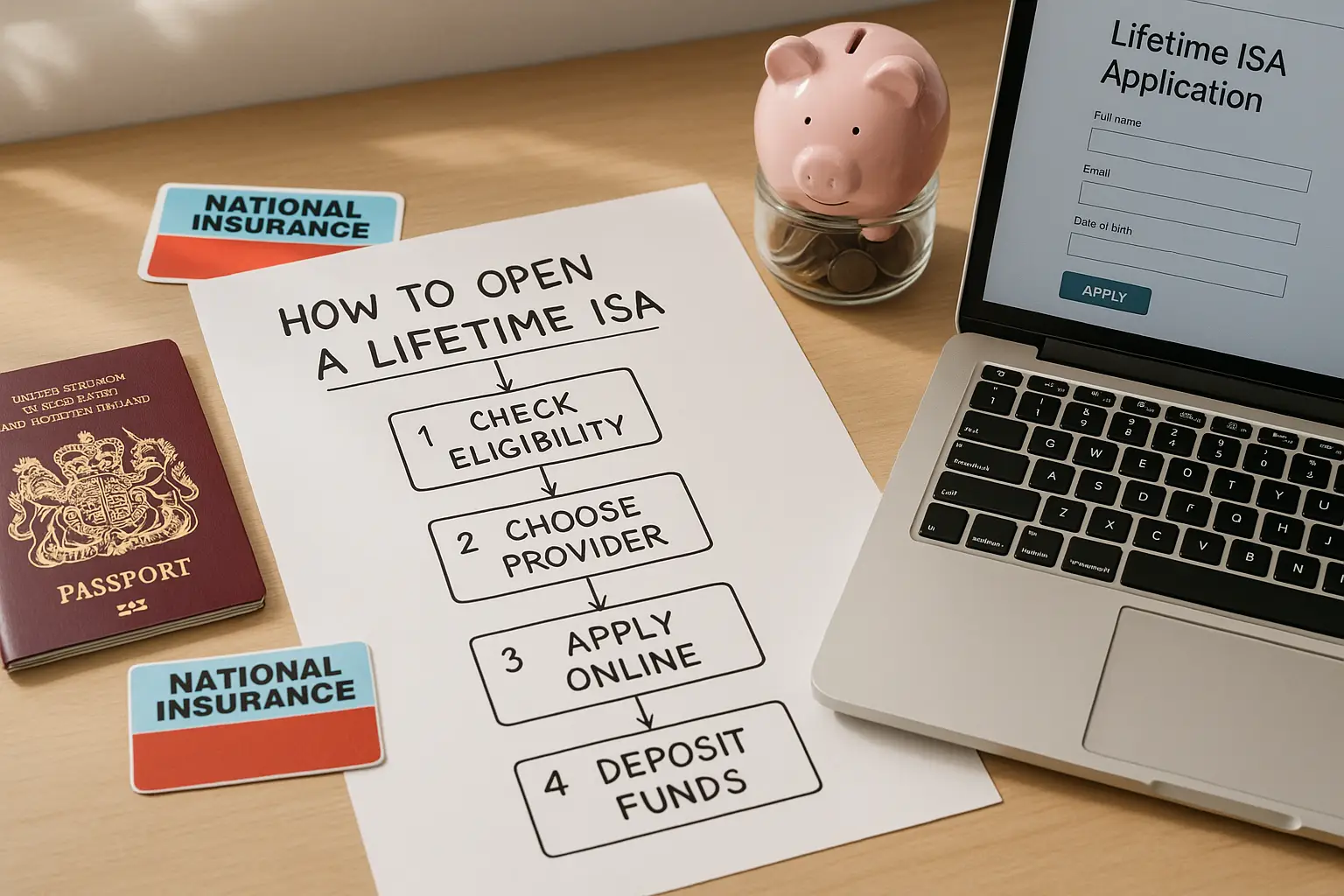

Strategies to withdraw safely

First, confirm eligibility: use for homes under £450,000 or wait until 60. Consider transferring to a standard ISA if needs change, avoiding the 25% hit (check our what is a lifetime isa guide). Life hack: Track contributions via apps to plan bonus-maximizing withdrawals without penalties.

What to do if penalized

Contact your provider immediately for charge details and appeal to HMRC if the withdrawal qualified (e.g., overlooked home purchase). Provide evidence like solicitor letters; successful appeals refund the penalty plus interest. For more, see EQI’s withdrawal guide.

Ongoing reforms and changes

Rising penalties have sparked calls to scrap or ease LISA rules, especially post-2025 Budget, amid housing pressures. No major changes yet, but monitor HMRC updates. For the latest on best lifetime isa options, explore providers adapting to trends.

Frequently asked questions

What is the penalty for withdrawing from a Lifetime ISA?

The standard penalty is a 25% charge on the withdrawn amount, including the government bonus, applied by HMRC for non-permitted access before age 60. This means savers lose more than just the bonus, often netting less than their original deposit. For context, in scenarios like emergencies, this lifetime ISA withdrawal penalties UK rule protects the scheme’s intent but can surprise users—always calculate via provider tools for exact impact.

Can I withdraw from my Lifetime ISA without penalty?

Yes, penalty-free if for a first home up to £450,000, after age 60, or terminal illness. These exceptions ensure funds serve homebuying or retirement goals without HMRC lifetime ISA withdrawal penalties. Beginners should verify with documents; experts note transfers to flexible ISAs as a workaround, though bonus is lost.

How much is the Lifetime ISA withdrawal charge?

It’s 25% of the total withdrawal, covering contributions and bonus, so a £10,000 draw incurs £2,500 charged. This rate, set since 2017, aims to deter misuse but has drawn criticism as penalties hit £102 million in 2024/25. Advanced users compare: it equates to a 6.25% loss on original savings (25% of 25% bonus), highlighting risks in volatile markets.

What counts as a first home purchase for Lifetime ISA?

A first home is your initial property ownership, valued at £450,000 or less, bought via standard sale or shared ownership (not rent-to-buy). You must not have owned a home before, and funds must be used within 90 days. This definition, per GOV.UK, prevents lifetime ISA early withdrawal penalties for genuine buyers but excludes investment properties—check residency status for edge cases.

When can I withdraw from Lifetime ISA after 60?

After turning 60, you can withdraw any amount anytime, fully tax-free, including all growth and bonuses. No restrictions apply, making it a flexible retirement pot. For those nearing eligibility, consolidate via lifetime isa rules 2025 to maximize; risks include market dips if in stocks version.

How have Lifetime ISA penalties trended in recent years?

Penalties rose 35% to £102 million in 2024/25 from £75.5 million prior, impacting 129,000 vs. 100,000 savers, per HMRC data. This surge ties to housing affordability issues, prompting reform talks. Experts advise diversifying savings to mitigate; beginners track via annual statements to avoid unintended lifetime ISA withdrawal penalties UK.

Can I appeal an HMRC Lifetime ISA withdrawal penalty?

Yes, appeal within 30 days to HMRC via your provider, submitting proof like medical certificates or home deeds. Success rates vary, but valid claims refund the charge plus interest. This process underscores enforcement rigor—strategize by documenting all withdrawals for quick resolution.

Are there changes to Lifetime ISA withdrawal rules in 2025?

No confirmed changes post-Budget, but rising penalties fuel discussions to raise home caps or ease bonuses. Monitor GOV.UK for updates; current 25% rule persists. For intermediates, this stability aids planning, but advanced savers hedge with multiple ISAs.