What is the ISA allowance for 2025/26?

The ISA allowance for 2025/26 remains £20,000, allowing UK residents to save or invest this amount tax-free each tax year. This limit applies across all adult ISA types, helping you shield your money from income tax and capital gains tax. For context, HMRC defines an ISA as a tax wrapper that protects your savings and investments.

Overview of the £20,000 limit

At its core, the annual ISA allowance 2025 stands at £20,000, unchanged from previous years unless altered by the budget. This tax-free ISA allowance 2025 means you can contribute up to this figure without paying tax on interest, dividends, or growth. For example, if you earn £1,000 in interest from a savings account outside an ISA, basic-rate taxpayers pay 20% tax on it, but inside an ISA, it’s all yours.

According to official guidance from GOV.UK, this limit resets every tax year, so plan your contributions wisely to avoid wasting any unused allowance, which doesn’t carry over.

Tax year start and end dates

The 2025/26 tax year begins on 6 April 2025 and ends on 5 April 2026, giving you a full 12 months to use your ISA allowance 2025/26. Mark these dates to maximise your tax-free savings—contributions made before 6 April count towards the previous year. This structure, set by HMRC, ensures savers align their finances with the fiscal calendar.

Who is eligible?

Eligibility for the UK ISA allowance 2025 requires you to be a UK resident aged 18 or over. Non-residents or those under 18 generally can’t open new ISAs, though existing ones may continue. Always check your status with HMRC, as Crown employees abroad might qualify under special rules.

Cash ISA allowance details

The cash ISA allowance 2025/26 falls within the overall £20,000 limit, with no separate cap currently in place, making it a safe haven for low-risk savers seeking tax-free interest.

Current cash ISA rules

Under current rules, the cash ISA allowance unchanged 2025/26 means you can deposit up to £20,000 into cash ISAs without tax on interest. These accounts function like regular savings but with tax protection—ideal if inflation outpaces your returns elsewhere. Flexible cash ISAs, introduced recently, let you withdraw and replace funds within the same year without dipping into your allowance.

For detailed rules, see MoneySavingExpert’s ISA guide.

How it fits within the total allowance

Your cash ISA contributions count towards the total ISA allowance 2025, so if you put £10,000 in a cash ISA, only £10,000 remains for stocks and shares or other types. This combined approach encourages diversification while keeping everything tax-free. Track your total subscriptions via your provider’s statements to HMRC.

Interest rates and options

Cash ISA rates vary, often beating standard savings accounts post-tax—shop around for the best deals. Fixed-rate options lock in rates for stability, while variable ones offer flexibility. Compare providers to ensure your money works harder.

Quick tip: Shop smarter for cash ISAs

To avoid common mistakes, use comparison sites and check for introductory bonuses. This life hack could boost your returns by 0.5% or more annually, saving you tax and fees.

| ISA Type | 2025/26 Limit | Key Rules |

|---|---|---|

| Adult (Cash, Stocks & Shares, etc.) | £20,000 | Total across all types; tax-free growth |

| Junior ISA | £9,000 | Separate from adult; for children under 18 |

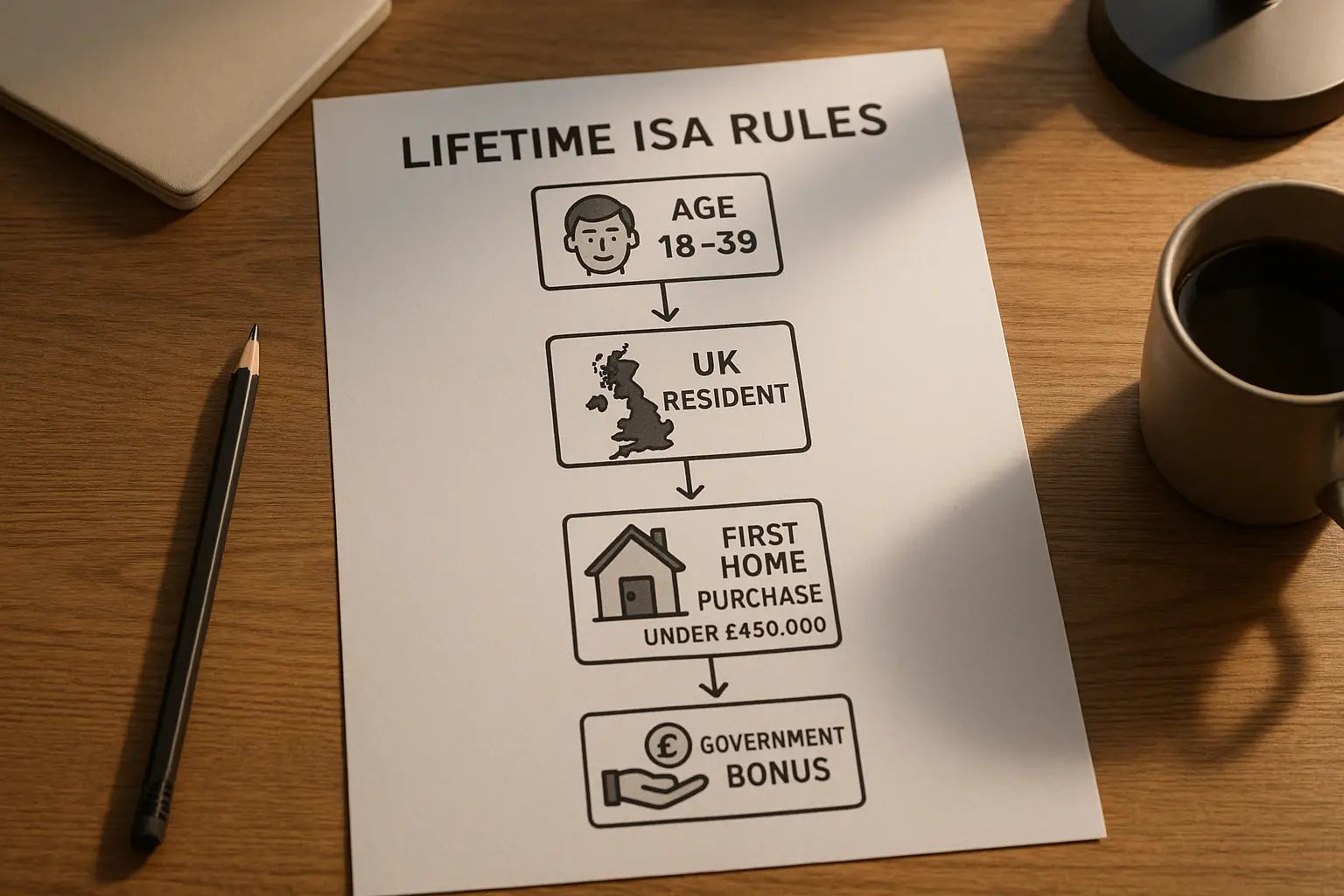

| Lifetime ISA | £4,000 (within £20,000) | Government bonus for first home or retirement |

Junior ISA allowance for 2025

The junior ISA allowance 2025/26 is £9,000, a dedicated tax-free pot for children’s future savings, separate from adult limits.

£9,000 limit explained

Parents or guardians can contribute up to £9,000 annually to a junior ISA, which grows tax-free until the child turns 18. This limit, per GOV.UK, applies to cash or stocks and shares versions. Unused allowance doesn’t carry over, so consistent contributions build wealth steadily.

Parental contributions

Anyone can contribute to a child’s junior ISA, not just parents—grandparents too—as long as total stays under £9,000. This spreads the tax-free benefits across family. The child gains control at 18, making it a smart, long-term hack.

Long-term benefits

Over 18 years, compound growth in a junior ISA can significantly outpace taxable accounts, avoiding up to 45% tax on gains. It’s a low-effort way to teach saving while securing their future.

Potential changes to ISA allowance in 2025 budget

While the ISA allowance 2025 remains £20,000 for now, budget announcements could alter this—stay informed to adjust your plans.

Rumors of reduction to £10,000

Reports suggest the government may cut the cash ISA allowance to £10,000 in the Autumn Budget 2025 to encourage investment. This speculative change, based on LBC news, aims to shift savers towards stocks but would limit safe options. Note: This is unconfirmed and requires official verification.

Impact on savers

A cut could squeeze conservative savers, forcing diversification or reduced tax-free savings. Higher earners might feel it most, losing protection on larger sums. Diversify now to mitigate risks.

What to watch for

Monitor the Spring Budget 2025 ISA allowance updates via HMRC or news. If changes hit, existing ISAs stay protected, but new contributions adjust. Act early to lock in current rules.

How to maximize your ISA allowance

To get the most from your ISA allowance 2025, spread contributions across types and use transfers strategically—here’s how.

Splitting across ISA types

Divide your £20,000: say £10,000 in cash for safety and £10,000 in stocks for growth. This balances risk while staying tax-free. Learn more about types of isa uk for options.

Transfers and withdrawals

Transfer between ISAs without affecting your allowance—ideal for better rates. Flexible ISAs allow same-year withdrawals and replacements, per GOV.UK’s tax-free savings newsletter. Avoid non-flexible ones to prevent allowance loss.

- Check provider transfer fees.

- Time moves before year-end.

- Understand what is an isa

- what is an isa for basics.

Common mistakes to avoid

Don’t exceed £20,000 or forget the tax year reset—overcontributions incur penalties. Track via apps to stay compliant. For top picks, see our guide on best isa uk rates.

Frequently asked questions

What is the ISA allowance for 2025/26?

The ISA allowance for 2025/26 is £20,000 for adults, covering all ISA types like cash and stocks and shares. This tax-free limit, confirmed by HMRC, lets you save or invest without paying tax on earnings. It’s a powerful tool for UK residents to build wealth efficiently, especially amid rising costs—start planning now to use it fully.

Will the ISA allowance increase or decrease in 2025?

Currently, no increase is planned, but rumors point to a potential decrease in the cash ISA allowance to £10,000 via the 2025 budget. This could push more people towards riskier investments, as per recent reports. Experts advise diversifying early; monitor official announcements to adapt your strategy without panic.

How much can I put into a Cash ISA in 2025?

You can contribute up to £20,000 to a cash ISA in 2025, as part of the total allowance, with interest fully tax-free. Rates currently hover around 4-5%, beating taxable savings for most. For beginners, opt for easy-access accounts; intermediates might prefer fixed terms for higher yields—always compare to maximize returns.

What is a Junior ISA allowance?

The junior ISA allowance is £9,000 per year for children under 18, separate from adult limits and tax-free until maturity. Parents or guardians open it, allowing family contributions for long-term growth. It’s beginner-friendly for securing kids’ futures, but consider access rules—funds lock until 18, promoting disciplined saving.

When does the 2025/26 tax year start?

The 2025/26 tax year starts on 6 April 2025, aligning with the UK’s fiscal calendar for ISAs and taxes. This date resets your allowance, so contribute strategically around it. For advanced users, time bonuses or transfers just before to optimize; check GOV.UK for exact deadlines to avoid missing out.

Can I contribute to multiple ISAs in 2025 and what is the maximum ISA allowance 2025?

Yes, you can split contributions across multiple ISA types up to the maximum ISA allowance 2025 of £20,000 total. This flexibility suits diverse portfolios—cash for security, investments for growth. Risks include overcomplicating tracking; use one provider if possible, and consult rules on transfers to compare advanced options like Lifetime ISAs.

For more on ISA limits and rules from Hargreaves Lansdown, visit their guide. Remember, this isn’t personal advice—consult a professional for your situation.